Why SMID-Caps: Broaden the Foundation U.S. Equities

Small- and mid-cap equities (SMID-caps) broaden the foundation of the U.S. market—companies that have grown beyond small-cap volatility but retain the agility to expand earnings faster than their large-cap peers. These firms often sit in their most productive phase of capital efficiency, where balance-sheet flexibility and reinvestment drive long-term compounding.

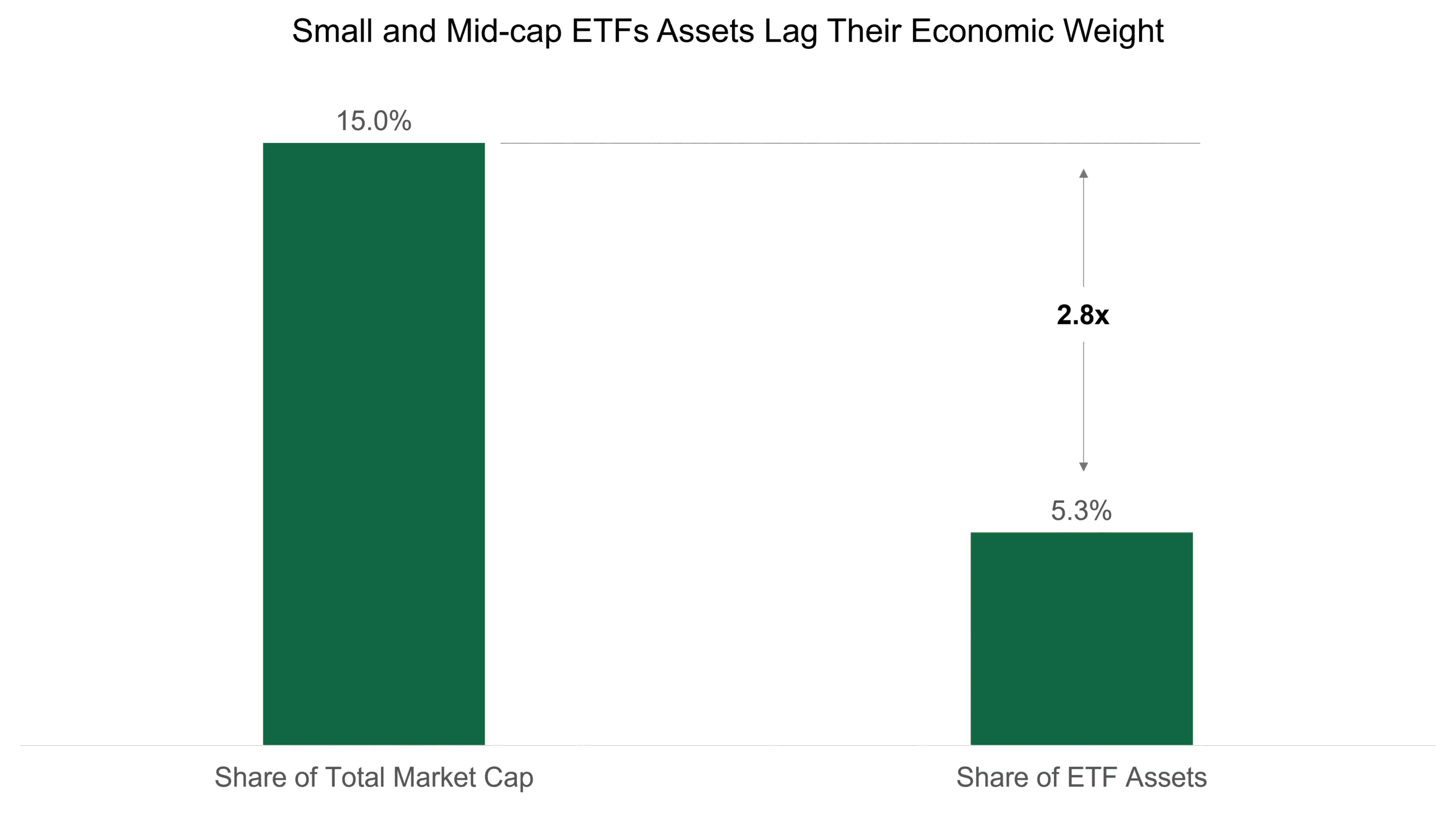

Although SMID-cap companies represent roughly 15% total U.S. market capitalization, they account for only about 5% of equity ETF assets — a meaningful underweight that leaves ETF portfolios heavily tilted toward the largest names in the S&P 500. This concentration limits diversification and heightens exposure to a narrow set of mega-cap stocks. By contrast, the SMID segment adds breadth—offering more balanced sector representation, higher stock dispersion, and a stronger foundation for systematic rebalancing (Figure 1).

Figure 1: Underrepresentation of SMID Cap Core in ETF Assets

Why Now: The Business-Cycle and Valuation Case

Historically, small- and mid-cap stocks have demonstrated their strength when market leadership extends beyond the largest companies—not only after recessions, but also during periods of rising investor confidence that prompt renewed interest in value outside of large caps. Across past cycles, smaller-company indexes have tended to lead when market leadership broadens and their valuation discount narrows.

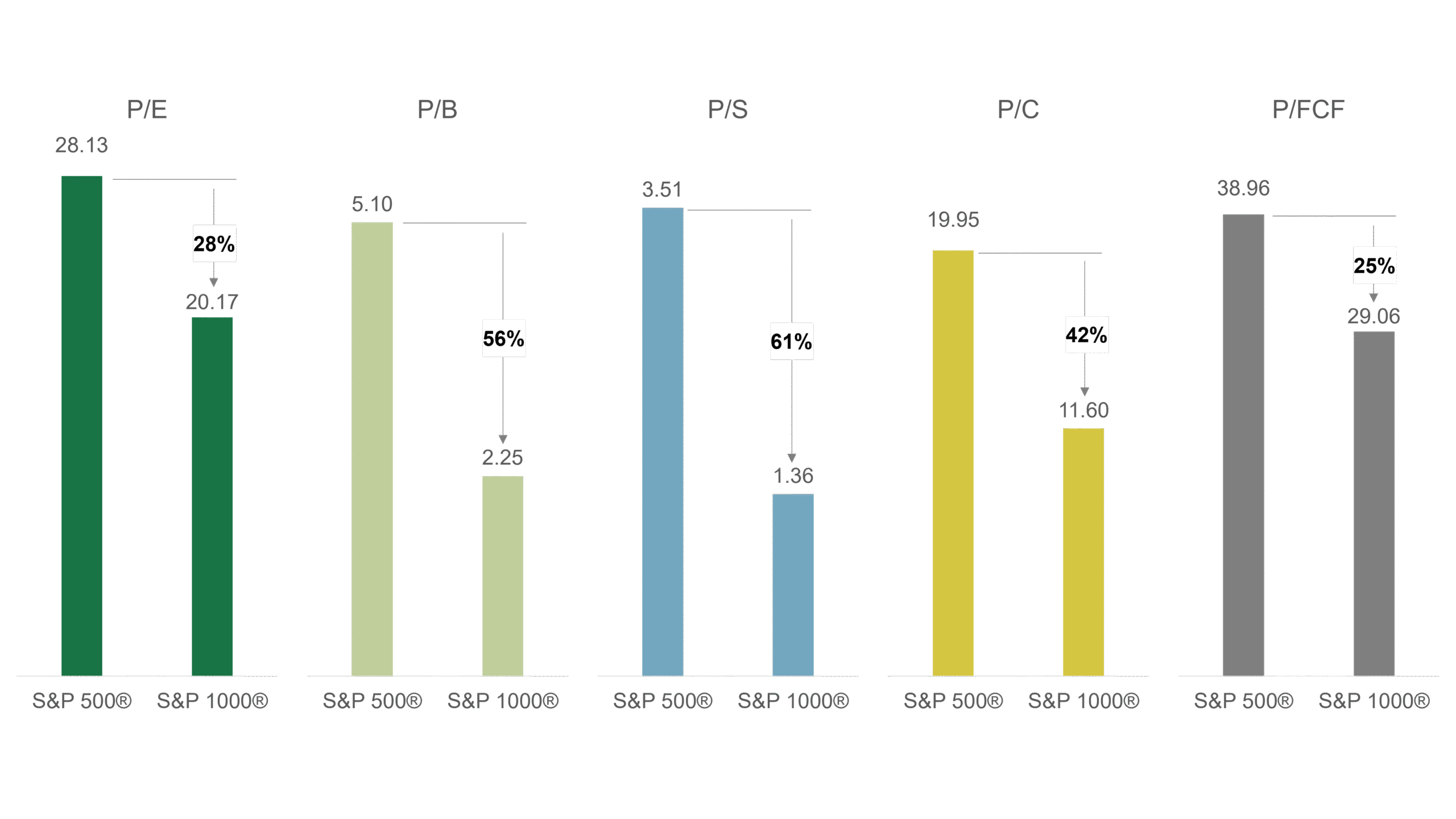

oday, SMID-cap valuations trade at a sizable discount to large caps, and should earnings growth narrow relative to those of large stocks, SMID-cap stocks present meaningful upside potential. Catalysts of that narrowing are emerging. Credit spreads remain stable, manufacturing PMIs are back in expansion territory, and SMID-cap earnings are positive. Other tailwinds include pro-growth policies in the One Big Beautiful Bill Act and a pickup in public offerings and mergers and acquisitions. Valuations remain compelling for investors—the S&P 1000 trades at nearly a 30% discount to the S&P 500 (Figure 2). For advisors, that creates both cyclical conditions and structural rationale to revisit this under-owned core.

Figure 2: Large Cap vs. SMID-Cap Valuation Metrics

Restoring Breadth: A View from Intech

In a recent Barron’s interview discussing the growing importance of small- and mid-cap companies in restoring balance to U.S. equity portfolios, Dr. Jose Marques, CEO of Intech, said, “Given the level of concentration that we have in the S&P 500, that seems prudent. The AI trade is a freight train.”

The article highlighted that even so-called “broad” indexes like the S&P 1500® mirror the same concentration challenges found in the S&P 500®. Intech’s view—expressed through its diversified ETF lineup—is that investors can address these imbalances by pairing large-cap exposure with deliberate breadth across smaller and midsize companies.

“Given the level of concentration in the S&P 500, that seems prudent. The AI trade is a freight train.”

Dr. Jose Marques, CEO, Intech, quoted in Barron’s

Why SMDX: Engineered for Breadth and Scale

SMDX applies Intech’s diversification-weighted design to the S&P® Small-Mid Cap universe—combining the simplicity of indexing with the discipline of systematic rebalancing. The result is broad, benchmark-aligned exposure that seeks to turn market volatility into an advantage rather than a source of risk.

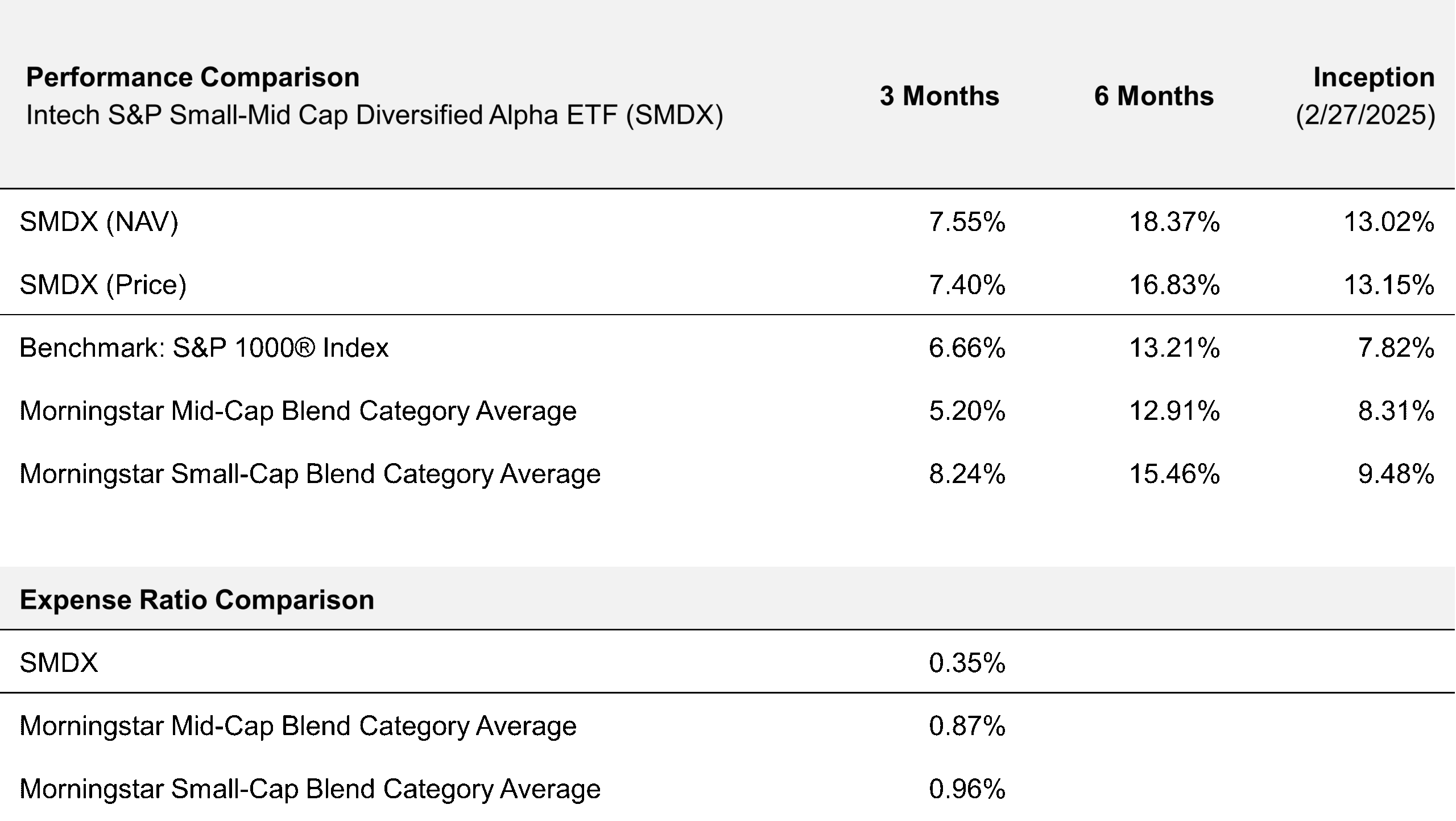

Since its launch, SMDX has generated competitive results relative to its benchmark and average peer through September 30, 2025 (Figure 3). The fund’s early results reflect Intech’s philosophy: structural diversification and disciplined rebalancing can enhance index efficiency without drifting from core beta exposure.

Figure 3: Performance vs. Benchmark and Morningstar Category Averages as of September 30, 2025

The performance data shown represents past performance and does not guarantee future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Returns for periods shorter than one year are not annualized. For the most recent month-end performance data, please visit IntechETFs.com. Please read the prospectus or summary prospectus carefully before investing.

To learn more, view current standardized performance and access fund materials at IntechETFs.com/SMDX.

Conclusion: Revisiting the Core

SMID-cap equities occupy an essential but often overlooked position in diversified portfolios—bridging large-cap concentration and small-cap volatility. With valuations still attractive and market breadth beginning to expand, investors have a window to restore balance across the equity spectrum.

SMDX offers a research-driven way to access that balance: a transparent, systematic ETF built for scalability and efficiency. For advisors constructing resilient core portfolios, it represents a timely opportunity to re-engage the broad engine of U.S. market growth.