For years, the core equity debate has been framed as a binary choice:

Passive or active.

Low cost or high conviction.

Index tracking or manager insight.

Rules-based or discretionary.

It’s a clean narrative.

It’s also incomplete.

The real differentiator in core equity may not be whether a strategy is passive or active — but how the portfolio is structured beneath the label.

The Industry’s Simplified Debate

The passive revolution brought scale, transparency, and cost discipline to core allocations. Cap-weighted indexing made broad market exposure efficient and accessible.

Active management promised differentiated returns through research, conviction, and insight.

Both approaches solve meaningful problems. Both have limitations.

But neither fully addresses a structural question:

How is risk distributed inside the portfolio?

When concentration, correlations, and rebalancing mechanics shape outcomes as much as stock selection does, the passive-versus-active framing may overlook a more fundamental distinction.

Cap-Weighted Indexing: Efficiency with Embedded Trade-Offs

Cap-weighted benchmarks are elegant in their simplicity. They allocate more capital to larger companies, reflecting the market’s own pricing.

That structure delivers:

- Low turnover

- Transparent exposures

- Close alignment to market beta

But as capital accumulates in benchmarks, weight concentration becomes structural. The largest companies increasingly dominate risk contribution and return influence.

The result is not inherently flawed, but it is specific. It is a design choice.

When market leadership narrows, cap-weighted portfolios may naturally concentrate risk in a small group of names. Diversification exists by count, but influence can skew heavily toward the largest constituents.

This is not a critique of indexing. It is an acknowledgment of structure.

Equal-Weight Variations: A Different Kind of Concentration

Equal-weighted strategies attempt to rebalance concentration by allocating capital evenly across constituents.

On the surface, that appears more diversified.

But equal weighting introduces its own structural tilts:

- Greater exposure to smaller companies

- Higher portfolio turnover

- Increased sensitivity to volatility

In redistributing capital away from mega-cap concentration, risk shifts toward size and volatility characteristics.

Again, this is not a flaw. It is a structural trade-off.

Diversification changes form. It does not disappear.

Factor Strategies: Systematic, But Cyclical

Factor-based strategies were designed to systematize active risk. They organize exposure around persistent characteristics such as value, quality, or momentum.

They offer:

- Transparent rule sets

- Academic grounding

- Defined return drivers

But factor definitions can potentially become crowded. Cyclicality can intensify. And correlations between factors can shift abruptly across regimes.

When capital concentrates around similar definitions of value or quality, diversification benefits may erode. What began as differentiated exposure can become synchronized behavior.

The challenge is not factor investing itself. It is that many factor approaches focus primarily on what traits to own, without explicitly addressing how those traits interact inside the portfolio.

Active Management: Conviction with Variability

Traditional active managers aim to outperform through security selection and differentiated positioning.

The benefits are clear:

- Flexibility

- Research depth

- Tactical opportunity

But active portfolios often depend heavily on discretionary judgment and implementation style. Style drift, benchmark aversion, and concentrated conviction positions can increase variability of outcomes.

Results can be compelling in certain environments and challenging in others.

Again, this is not a flaw. It reflects the human element in portfolio design.

The Overlooked Dimension: Inclusion vs. Interaction

Across passive, equal-weight, factor, and active approaches one common thread emerges. They attempt to answer the question:

What should we own?

Fewer explicitly address:

How do the holdings interact?

Portfolio outcomes are shaped not only by stock fundamentals, but by:

- Weight distribution

- Volatility dispersion

- Correlation structure

- Rebalancing discipline

Inclusion determines which companies are in the portfolio. Interaction determines how risk behaves over time.

When leadership rotates, correlations compress, or dispersion widens, interaction effects can meaningfully influence results, even when the underlying holdings remain the same.

This interaction dimension often sits beneath the surface of the passive-versus-active debate.

Why Structure Matters in Core Equity

Core equity is expected to:

- Deliver benchmark-aligned exposure

- Provide scalable beta

- Operate within risk constraints

- Serve as a policy anchor

Because of that role, extreme tilts — whether concentrated or highly differentiated — may be difficult to justify within a fiduciary framework.

The challenge becomes:

- How do you maintain benchmark familiarity while distributing risk more deliberately?

- How do you avoid simply inheriting structural concentration?

- How do you introduce differentiation without abandoning policy alignment?

Those questions shift the debate away from labels and toward design.

A Structure-First Perspective

A structure-first approach begins at the benchmark, not in opposition to it.

It views portfolio construction as a two-dimensional problem:

- Which businesses to own

- How those businesses are assembled and maintained together

This perspective does not reject indexing. It does not dismiss active insight.

It reframes them within a broader architecture.

The goal is not to eliminate market beta. It is to govern how beta is expressed.

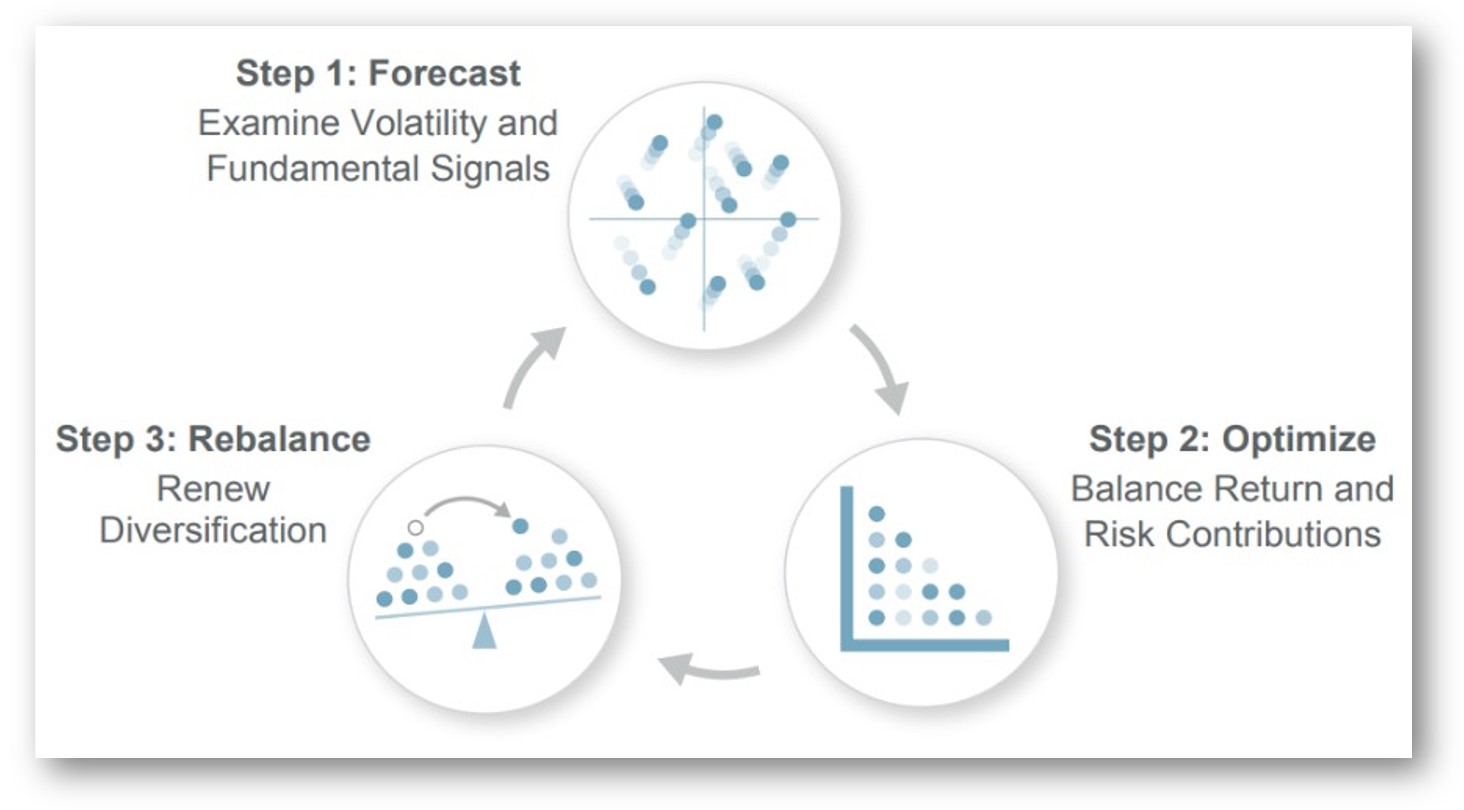

Rather than treating passive and active as opposing camps, structure-first design seeks to integrate:

- Fundamental information

- Portfolio diversification

- Controlled tracking error

- Systematic rebalancing discipline

All within benchmark-aware guardrails

The Debate Isn’t Binary

The future of core equity may not be passive versus active.

It may be:

- Passive.

- Active.

- Or structurally engineered.

In a market where concentration and correlation patterns evolve rapidly, portfolio design becomes as important as portfolio selection.

When fiduciaries evaluate core allocations, the most important question may no longer be:

“Is this passive or active?”

It may be:

“How is risk structured inside this exposure?”

Compare the Approaches

Explore how a structure-first framework differs from conventional indexing, factor models, and traditional active management — while remaining benchmark aligned.

Compare Approaches → Intech | The Architecture of Diversified Alpha