Look Back: What Changed in Q1

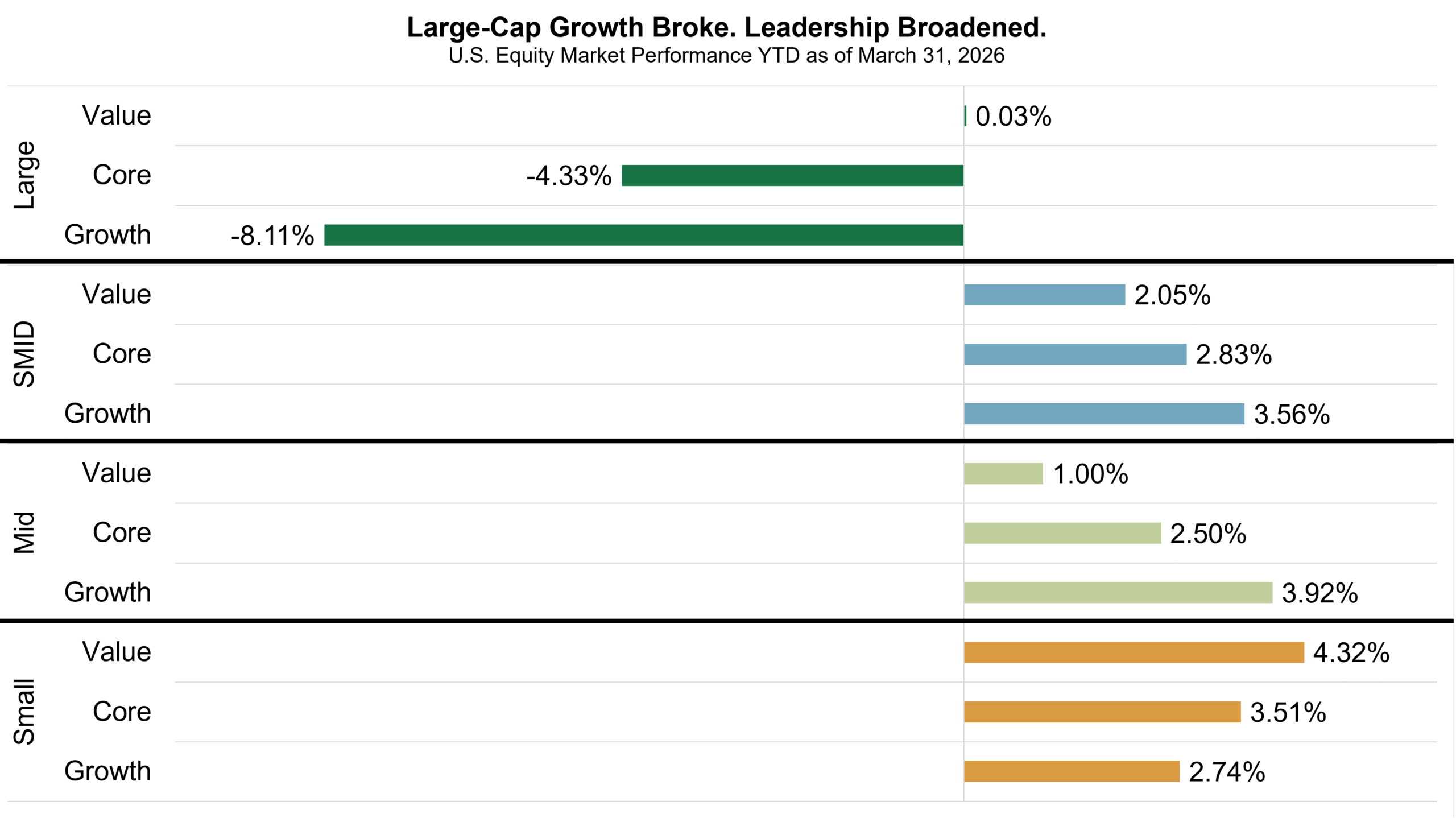

The headline shift was clear. U.S. large-cap indices led market declines as late-quarter geopolitical escalation accelerated an abrupt rotation away from mega-cap growth. The Nasdaq-100 fell 5.82%, and the S&P 500 declined 4.33%. In contrast, other parts of the capitalization spectrum proved more resilient. The S&P MidCap 400 gained 2.50%, the S&P SmallCap 600 rose 3.51%, and the S&P 1000 advanced 2.83% for the quarter.

Style leadership changed as well, but the pattern across the S&P family was more nuanced than a simple value-over-growth headline. In large caps, the rotation was decisive: S&P 500 Growth declined 8.11% in the quarter, while S&P 500 Value was essentially flat at 0.03%. In mid-caps, however, growth led, with S&P MidCap 400 Growth up 3.92% versus 1.00% for S&P MidCap 400 Value. In small caps, value regained the edge, as S&P SmallCap 600 Value rose 4.32% compared with 2.74% for S&P SmallCap 600 Growth. At the broader S&P 1000 level, growth also finished ahead, up 3.56% versus 2.05% for value.

Figure 1. U.S. Equity Market Performance, Q1 2026

That mix of results points to a subtler conclusion. The quarter did not deliver a clean value-over-growth win across every capitalization tier. It did show a sharp break in large-cap growth leadership and a broader market preference for valuation support, cash-flow durability, and less concentration in the narrowest leadership cohort as energy prices rose and discount-rate pressure intensified.

The quarter also revealed a notable shift beneath the surface of the S&P 500. Year to date through March 31, the bottom half of stocks by market capitalization outperformed the top half by nearly 10% on a weighted-average-return basis. In a market that had been defined by narrow mega-cap dominance, that may represent one of the sharpest reversals of concentration in the last decade.

The move was not limited to the United States. International markets outside the U.S. were also generally down, with MSCI Europe falling 2.68%, MSCI EAFE down 1.12%, and MSCI Emerging Markets off 0.10%. Defensive minimum-volatility strategies helped limit losses in some cases, but results were mixed. The broader message was that the quarter was not a simple U.S. tech wobble. It was a global risk-off episode shaped by rising geopolitical stress and changing duration expectations.

Interpret: What the Quarter May Have Revealed

The returns mattered not just because they marked a change in leadership, but because they revealed how dependent many portfolios had become on a narrow part of the market.

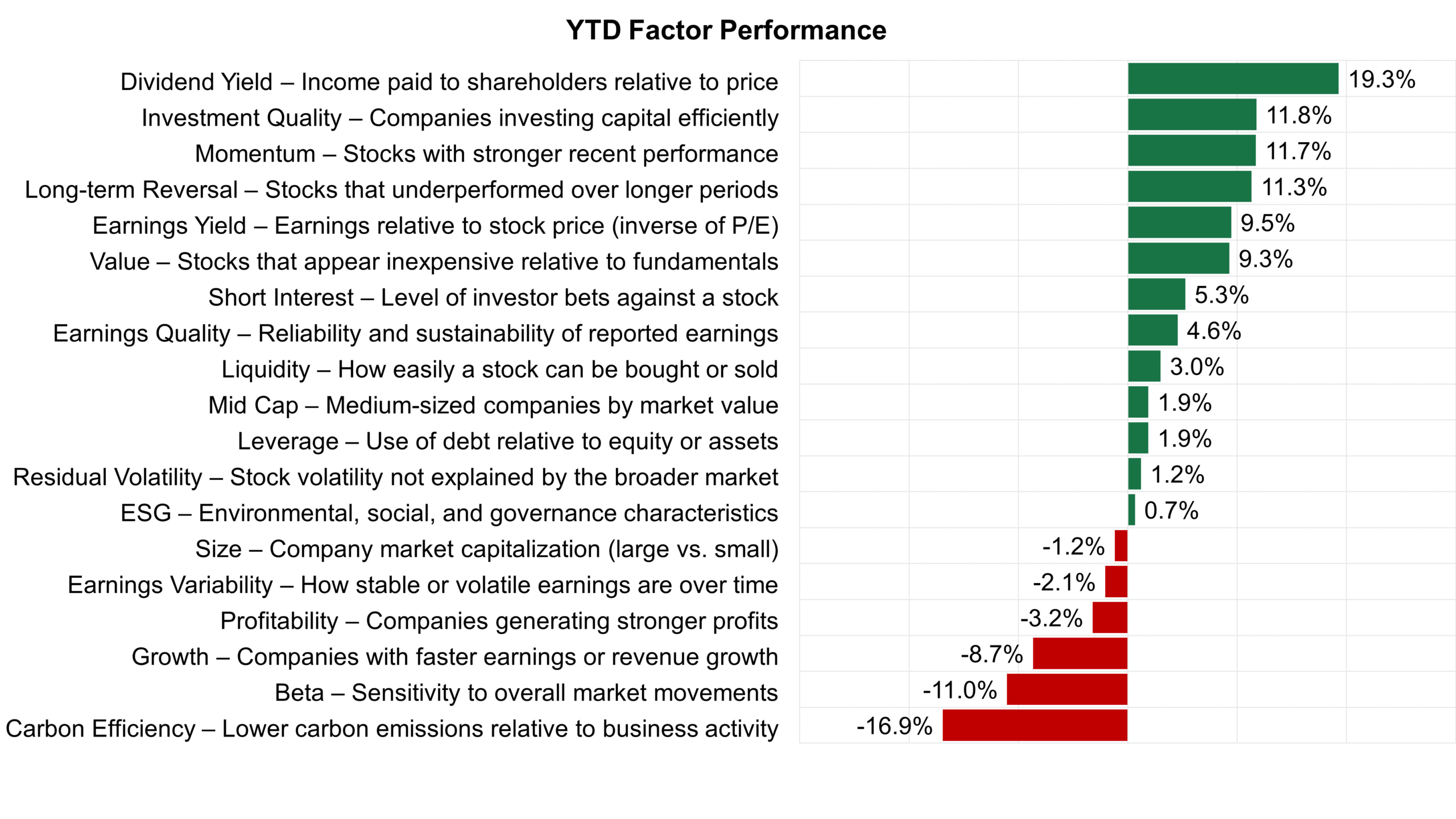

The factor backdrop was equally revealing. A Barra-style analysis of the MSCI World universe showed notable strength in dividend yield, which posted a spread of 19.29%. Investment quality added 11.76%, value gained 9.29%, and momentum rose 11.71% as leadership increasingly overlapped with defensive and value-oriented characteristics. At the same time, carbon efficiency fell 16.93%, beta lagged by 11.05%, and growth trailed by 8.65%.

Those factor moves did not occur in a vacuum. They widened sharply as military strikes involving the U.S., Israel, and Iran began in late February. As threats to the Strait of Hormuz emerged and oil prices surged above $113 per barrel, market mechanics shifted in real time. The conflict premium lifted energy exposures and redirected market preference toward cash-flow security, valuation support, and businesses perceived as more resilient to rising costs and higher discount rates.

Figure 2. MSCI World Factor Spreads, Q1 2026

That geopolitical context matters because it helps explain why long-duration growth came under pressure so quickly. Duration sensitivity had already become an important feature of market leadership. When oil rose and inflation risk re-entered the conversation, long-duration equities faced a double burden: a less friendly discount-rate backdrop and a market less willing to pay for concentration at any price.

In that sense, the quarter did more than rotate leadership. It revealed how dependent many portfolios had become on narrow, long-duration leadership.

That is the portfolio implication worth taking seriously.

For several years, many core allocations have benefited from a market structure in which a small group of dominant companies drove an outsized share of index return and risk. Over time, that concentration began to feel normal. Broad-market exposure still looked diversified on paper, but actual outcomes were increasingly determined by a much smaller set of companies, sectors, and characteristics.

Q1 did not prove that this structure is over. It did remind investors that it is more fragile than it appears.

And that may be the most important interpretive lesson of the quarter. Portfolios do not just reflect the market. They also reflect assumptions about how leadership persists, how discount rates behave, and how broad participation needs to be in order to matter. When those assumptions are challenged, even briefly, the gap between “owning the market” and “owning a balanced opportunity set” can reveal itself more clearly.

This backdrop may be relevant to how investors evaluate an approach that emphasizes diversification, breadth, and rebalancing discipline. The quarter favored characteristics associated with resilience, diversified participation, and less duration sensitivity. That is consistent with Intech’s broader argument that structural balance matters more when the market stops rewarding concentration as uniformly as it had before.

Look Forward: The Risk of Duration

The outlook is more useful when it does not force a single macro answer.

The case for near-term Fed rate cuts diminished as the 10-year Treasury yield climbed toward 4.4%. Rising oil prices tightened financial conditions, effectively doing some of the Fed’s work. At the same time, the economy remained relatively resilient. Labor markets were firm, consumer spending held up, and corporate balance sheets still offered some cushion against higher costs.

That leaves equity markets facing a bifurcated path, shaped more by the shock’s duration than by its existence.

Transient De-escalation

If tensions ease quickly and oil prices retreat, a key inflation headwind could fade just as the U.S. economy continues to show resilience. That would help stabilize discount-rate expectations, ease margin pressure, and reduce the need for markets to prize only defensive or cash-flow-heavy exposures. In that environment, growth-sensitive sectors could recover, and broader equity participation could strengthen from a firmer economic base.

Persistent Structural Shift

If the conflict persists and the supply shock becomes more structural, higher energy costs and tighter financial conditions could become a more lasting headwind. That would keep pressure on long-duration equities, elevate the importance of cash-flow resilience, and make concentration risk harder to ignore. In that setting, value-oriented exposures, defensives, and more balanced participation may continue to compare favorably.

That is why the risk of duration is such a useful frame for Q2.

Implication for Small- and Mid-Cap Stocks

The question is not simply whether investors should expect one segment of the market to win next. It is whether portfolios are prepared for a wider range of leadership outcomes if inflation sensitivity remains elevated and concentration proves less reliable than it was in the prior regime.

That is also where the implication for small- and mid-cap stocks fits naturally.

Not as a style trade. Not as a call that SMID stocks must lead from here. And not as a replacement for large-cap.

But as one possible way to think about participation.

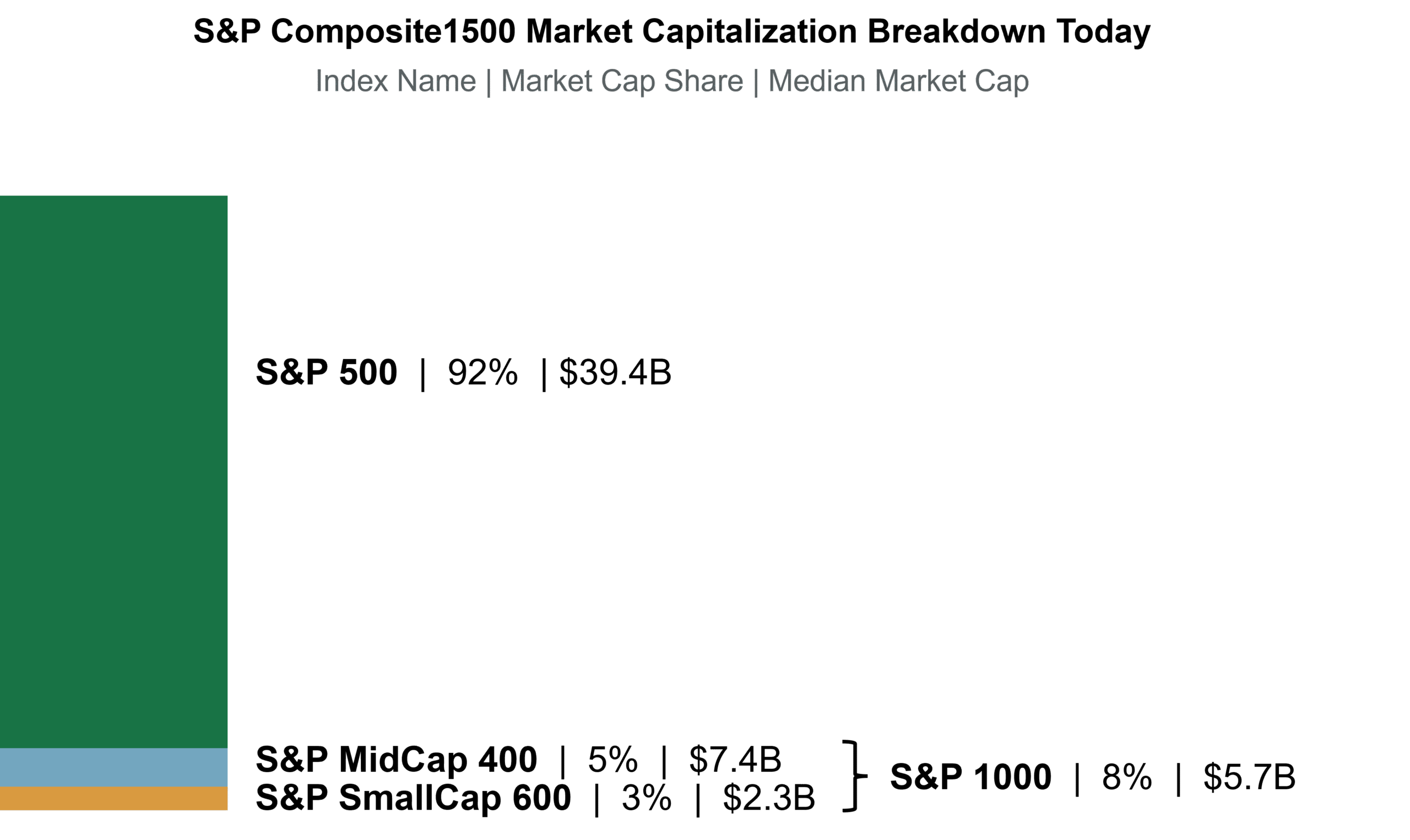

Figure 3. U.S. Equity Market Capitalization, Q1 2026

If leadership continues to broaden beyond the most concentrated large-cap cohort, advisors may want to evaluate whether portfolios have enough meaningful exposure to the part of the market where that broader participation becomes investable. In a cap-weighted world, inclusion is not the same as impact. Many portfolios already hold small- and mid-cap companies, but often not in enough size to influence outcomes if breadth improves meaningfully.

SMID represents a part of the market that potentially offers more direct participation if leadership continues to broaden, without requiring a wholesale rejection of large-cap exposure. In this context, it is best framed as a structural complement rather than a tactical pivot. And using the S&P family matters here: the S&P MidCap 400 and S&P SmallCap 600 both finished the quarter in positive territory, while the broader S&P 1000 gained 2.83%, reinforcing the point that resilience extended beyond the narrowest leadership cohort.

Final Thought

The most useful reading of Q1 may be the simplest one.

It was a quarter in which concentrated, long-duration leadership looked less stable. It was a quarter in which value, quality, and cash-flow resilience reasserted themselves. It was a quarter in which geopolitical risk mattered, factor leadership widened, and the market reminded investors that broad exposure can become less balanced than it appears.

That does not settle the next regime. But it does sharpen the question for Q2.

If market participation continues to broaden, are portfolios positioned to participate?